Recovering from "Lifestyle Creep": How I cut my cost of living by 75%

In 2016, I decided to see if I could go an entire year without buying any new clothes. I told myself I was trying to trim back on spending, but I was hardly making a dent. While I made it through the year without buying any new clothes, I was already the type of person that bought a winter coat for $50 as a silent protest against the people who were convinced that a $1000 Canadian Goose jacket was a good way to spend money.

I had cut expenses in an area in which I didn’t really spend recklessly to begin with. I was telling myself a story. That I was frugal. That I was not like everyone else. I had become victim of lifestyle creep.

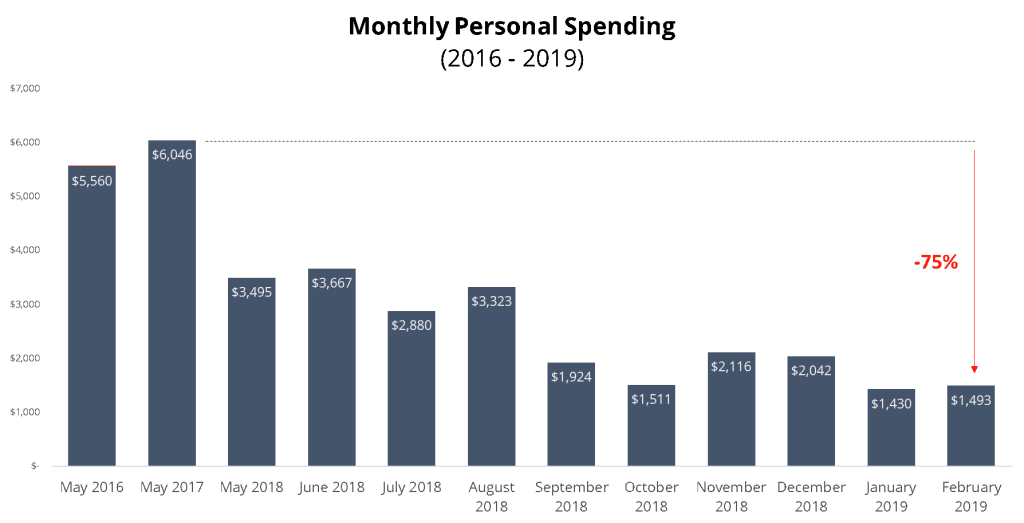

Two years ago, I was living in New York City working in a fancy six-figure job, spending more than $6,000 a month. It’s almost two years later and my personal expenses have been less than $12,000 for the last six months.

I’m not sharing my expenses with you to brag. Instead, I am trying to make sense of how I convinced myself that spending $72,000 a year was a normal thing to do.

This mindset was driven by the myth of a “steady income”

For most of the time I was employed full-time, I assumed that I would work in this manner for the rest of my life. What this meant is that I bought into the career story – the story that says the whole point of a career is to continue to grow and to keep making more money. I reflected last year on how I justified my spending:

A steady job meant my income on autopilot. Paychecks showed up in my bank account no matter what. Since I was lucky to have jobs that paid me much more than I needed, it led to a certain recklessness and willingness to pay for convenience because much of my time was spent at said full-time job. $300 for an Acela train to Boston to save 45 minute? Done. $75 dinners? Why not?

New York City is perhaps the most efficient city in terms of extracting wealth from people that want to pursue fun. Round-trip ride on the subway? $5.50. A couple drinks with a friend? $30. A “low-key” dinner? $45 A round of shots for friends? $55 Any income you earn? New York City and the State take an automatic 10% off the top.

New York City is a great place to have a lot of modern pleasure, but it sure as hell doesn’t care about how much you’re spending to do it.

When I Became Self-Employed, This Mindset Flipped

The cost of a thing is the amount of what I will call life which is required to be exchanged for it, immediately or in the long run.

Henry David Thoreau, Walden

As soon as I became self-employment I had the most obvious realization in the world.

The more I spend, the more I have to work

You’re thinking “WOW! Thanks Paul! What a knowledge bomb!”

I know, I know. On its face, its not all that insightful of an observation but if you think about the ways in which we actively ignore this fact, it become a bit more powerful.

There are a few mistakes I made:

First, bought into my own “career narrative” I implicitly assumed I would be working forever and never sat down to write down how much would actually be enough. Further, I had never in the first ten years of my career sat down to ask myself what kind of life I might want to live and what it might cost.

Second, I mentally framed my earnings and expenses like a company with a fiscal year-end. Wipe the slate clean and earn from scratch again. With this mindset, its easy to see how you end up with the fear that if you lose your income, you won’t be able to pay your expenses that month. Thise was somewhat confirmed to me when a person who I know has over $100k in savings said to me with a straight face “I can’t just quit my job, how would I pay rent?”

Third, since my entire life surrounded around work, I had no conceivable metric to value my money. I just had the vague sense that I shouldn’t spend too much. Now, having understood the benefits of leisure, I cringe with pain when I hear of someone spending 75,000 on a wedding. All I can think of is the fact that that money could easily pay for around the world travel for at least three if not four or five.

Shifting Behaviors

A month after leaving my job in New York, I moved to Boston. I realized that my self-employment journey wasn’t going to last long if I didn’t change my money habits. I also realized that I didn’t want to be constantly worrying about making enough money each month. I wanted to stretch my savings a bit longer. By changing some pretty basic things and calculating my “cost of a good life” (which I turned into a tool here), I was able to lower my monthly cost of living by almost $2,500.

In Boston, I stopped buying new things and started relying on sustainability exchanges like Buy Nothing and Freecycle. As my cost of living continued to go down and I gave away or sold most of my possessions, I felt a renewed sense of freedom creep back into my life.

In September of 2018, I moved to Taipei and have been living between Taiwan, Thailand and Indonesia for the past seven months. I’ve lowered my cost of living even further and it hasn’t all come from a difference in location.

As I started to design my life around working less, I also had a calmness and contentedness re-emerge in my life. I stopped drinking alcohol, craving expensive meals and opting for the nicer arrangements while traveling. I no longer “deserved” them after a long work-week. Nor did I need them.

I’ve come to believe that “financial security” as most people frame it is a myth. The problem with this idea is that there is never a number that is defined as “enough.” While some in the financial independent, retire early (FIRE) crowd are are literally defining how much is “enough”, it doesn’t seem to resonate with most people. Yet this community is often spot in with diagnosing the problem.

We are owned by our jobs and our stuff, not the other way around.

Join 25,000+ curious readers

Reflections on life, work, and what really matters