Die With Zero: Why Too Many Save Too Much for Too Late In Their Lives (Book Review)

If The Pathless Path is about deprogramming yourself from default work beliefs, Die with Zero by Bill Perkins is about deprogramming yourself from default money beliefs.

Die With Zero is an entertaining, persuasive, and useful book that argues that far too many people, “save tend to save too much for far too late in their lives.”

This is a hard topic to talk about, but Perkins does it well. Money is a topic where many people are better at saving than spending, including me. Our relationships to work and money are tightly linked and the more I think and read about these two things, the more I think that our money beliefs are foundational to our relationship to work. I don’t think you can have a good relationship with work without first interrogating and grappling with your money beliefs.

While I’ve questioned a lot of my beliefs around money, such as how I think about generosity, retirement, and fear, this book still challenged me in interesting ways. Most notably, it’s pushed me to dream a little bigger about how I’m spending my time right now and in the near future. It also nudged me to consider questions like

- Am I saving too much?

- What experiences might I not be able to take in ten years?

- What experiences might I enjoy a lot less in twenty years?

- How can I think about giving my children money earlier in their life when they have more time but not money?

If these questions excite you, the book will likely be a fun read.

Here are some other reflections from the book:

Takeaway #1: It reframes life away from purely a money problem to a life force problem

Many people look at life in clear, linear stages: youth, adulthood, and then retirement. This is less about any sort of life stage and more about how one fits in an economic system. It’s useful to know the world works like this but if we take the system’s economic goals for our own, we forget that we have a life to live.

Perkins pushes back against this tendency in the book, reframing life as a problem of life energy: “What’s the best way to allocate our life energy before we die?”

This is a push against the default or what he calls “autopilot.” Most people look at life and retirement as a money problem because, well, that is what everyone else is doing. By looking at life as a life energy allocation problem you might make different choices like giving money to your children while they are still alive, deprioritizing work and buying back time before you are “supposed” to retire, and spending lavishly on experiences that might pay “memory dividends” to you and people in your life.

His idea of a “personal interest rate” was useful for thinking through the tradeoffs you might make between life and money. This is just a way to “discount” future time and force you to think about the value of the present moment. It also means that the older you are, you should be way less willing to trade your time for money. This is because your life energy is becoming scarcer and thus, more valuable. Taking a full-time job with no vacation when you are 80 would be a tragic circumstance for most people. But what about 68? 60? When does the cost of the time you must give up become too high? These are the tricky calculations you must figure out yourself.

Many of Perkins’s friends tell him, “Well, I don’t like anything else,” or “I like work!” To which he replies, “How do you know what your tastes are if you haven’t done anything besides work or raise kids.” The message: dream a little bigger, you only have one life!

“You Takeaway #2: Retire on Your Memories”

As we get older, we spend more time reflecting on our lives. This is why Perkins argues that more people should think about old age as a combination of savings AND memories. Through this lens, having memorable experiences earlier in life, especially before retirement, can be valuable because they will pay memory dividends. And there’s good evidence that this is what makes people happy. I’ve written before about how the Nobel prize winner Daniel Kahneman abandoned studying happiness after realizing that “people don’t want to be happy the way I’ve defined the term – what I experience here and now.” Instead, he thought that people want to be satisfied by the “story they tell about their lives.”

For several years before my grandfather passed away, I increased the amount of time I spent with my Nana. This was a conscious decision. After I lost my grandfather suddenly in 2010, I knew that I wouldn’t have much time left with her. I also really enjoyed her company. She seemed to really understand me and always was excited to hear about my life. In 2018 before I moved to Taiwan, I set a goal of spending fifty days with her over the summer.

I was only one year into self-employment and was barely covering my cost of living at the time, but I had the sense that time with my grandmother was far more valuable than any money I might earn. I was buying time with money (or at least potential money). It’s easy to see the logic in Perkins’s argument to make these kinds of decisions because there is literally no amount of money you could pay me to erase these memories from my life.

Takeaway #3: Periods of our lives are finite

I recently became a father. I’ve entered the period that Khe Hy calls the “magic window” – the period of 10-12 years where your children think you are the greatest thing on earth. There are experiences I can have with my family right now that I will not be able to have when they are older. But this is also true no matter what phase of life we are at. I can’t live my twenties again (where I wish I had quit working full-time a lot earlier). And I won’t get a do-over on my 30s (which I’m a little happier with how I spent my time).

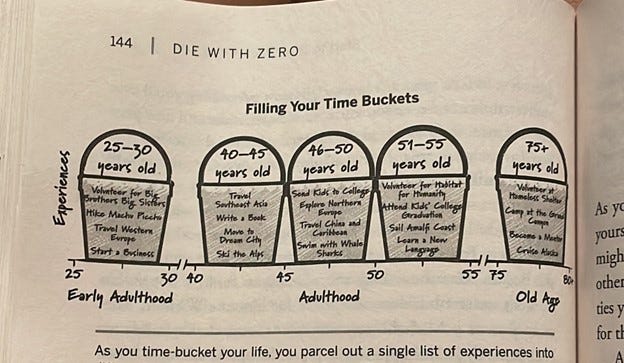

An exercise he proposes to help people become more aware of these expiring periods is doing a “time bucket” reflection. Here is Bill’s own reflection from the book:

I like this for two reasons. First, it’s a generative exploration of possibility. Angie and I often do exercises like 5-Year “dream life” plans and others where it nudges us to imagine things we aren’t thinking about already. It’s always fascinating how easy it is to come up with ideas outside of our current imagination and realize how few people ever spend 15 minutes trying such things.

The second I like about this exercise is it might help you realize experiences that are worth waiting on – like in Bill’s case an Alaskan cruise in his 70s. I feel similar! A cruise now? Eh. But in my 70s? Maybe!

In my travel around the world, I saw so many elderly people traveling who struggled to walk and more. I’ve increasingly thought that at that age maybe it’s time to retire to a reading nook and give up travel. Which makes me want to travel and live abroad in the coming decades with my children, during the years I’ll never be able to relive.

Many of us see travel as part of the deferred life plan. We will travel when we retire. That’s just what you do. Die With Zero offers many helpful reframes, but this quote stuck with me the most: “How much do you think you’ll enjoy climbing Rome’s Spanish Steps when you’re in your nineties?

Takeaway #4: Don’t Trade Years of Your Life for A Hospital Bill at The End of Life

“But healthcare!!”

In the US this is a common reason people have for saving as much as possible for retirement. But I think what is really happening is that they are picking the most convenient excuse to not have to deal with their underlying money insecurities. Saying you are worried about healthcare costs sounds smarter than saying you fear dying and running out of money (or at least is more accepted at a dinner party).

The thing is you can pull data on all of this. There are tons of it. A few I found quickly:

- “In the U.S., only 1 percent of hospital care at the end of life is paid for out of pocket” (Richmond Federal Reserve)

- Only around 30% of people die in hospitals (Reuters)

- If you do save you can buy long-term health insurance with predictable costs

- Increasing numbers of people are choosing to die in hospice

- Most Americans (and people in other countries) are not only covered by government healthcare but also have steady income via things like social security

But even without the data, someone might be able to point to an extreme example where someone’s family went bankrupt from medical issues. But Perkins is not saying that healthcare costs are never high – he’s saying that people should think about what they are trading off to save as much as possible for when they are old. Is it worth working several more years of your life, withholding life-changing gifts from people, or giving up meaningful life experiences all for having to potentially extend your life another month at the tail end of your life? Probably not and it’s likely not going to cost as much as you think.

And there are clear data that people do save too much in the US. Nick Maggiuli’s book Just Keep Buying pointed out that in any given year, “58 percent of retirees withdraw less than their investments earn.” The result? He writes, “The average retired adult who dies in their 6os leaves behind $296k in net wealth, $313k in their 70s, $315k in their 8os, and $238k in their 90s.”

The biggest problem with claiming to care about healthcare expenses is that it implies you are prioritizing your health. However, Perkins would just say: if you really cared, why not spend it on a personal trainer right now?

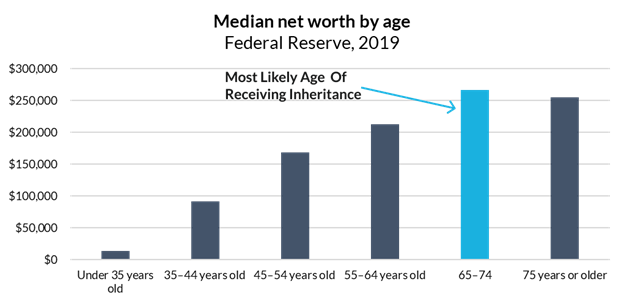

Takeaway #5: Inheritance is wasted on the elderly because they have enough money but not enough time or health

“But I want to leave an inheritance for my kids!”

Perkins gets pretty fired up about this. He often tells his friends they are hypocrites. They “aren’t putting their children first but instead are treating their kids as an afterthought.” The reason is simple: “A person’s ability to extract real enjoyment out of the gift declines with age.”

In the US, 80-90% of wealth transfers are inheritances and the most likely time this occurs for people is sometime in their 60s. What also happens in our sixties? People tend to read their highest point of wealth. We can see this clearly by looking at median net worth data from the Federal Reserve in the US.

Perkins writes about giving his grandmother $10,000 when he had “made it” in his career. She was in her 70s and had little use for it. She had a simple life and didn’t end up spending any of the money. This taught him that it was probably better to try to create memorable experiences for the people in his life, or at minimum give gifts to people earlier in their lives.

And this is the other side of an inheritance. He argues that thinking only about money is a cop-out. Parents should think about the inheritance of memories that they wish future generations to have. What are the life-changing gifts one could make during someone’s life? What are the experiences that might seem extravagant, but people would talk about for years? The odds are if you see your relationship with your kids as something that is “solved” through a transfer of money, it’s already on shaky ground. You’d be better off trying to turn at least some of that money into memories.

Because we tend to spend less as we age and the upsides of being able to spend money intentionally earlier in life are higher, Perkins believes the ideal age to give children an “inheritance” is sometime between 25-35 years old. This is because they are money-poor but time and health rich. They can create experiences or take risks that they would not be able to otherwise take when older. Of course, this is hard. As I’ve written about with work, we have DEEPLY embedded scripts that people need to learn how to struggle their way through their work lives. I suspect this is more of a cope from an industrial era where you really did need to put your time in. My parent’s generation had to work twenty years to get 4 weeks of vacation. Success really was downstream of time. This is no longer true and the suffer=good script is holding us back in how we think about work AND money.

Angie and I received a small gift when we had our daughters from Angie’s parents, and it was not at all something I was expecting. It was a profound gesture and really made us think more deeply about how we can proactively use that money to spend more time in Taiwan, help her parents travel, and create amazing experiences for our daughter.

But if you don’t want to give to your kids? Fine. The point still stands – spend the money now. Give it to a charity. Create life-changing experiences. Because if you’re leaving it behind you’re already elderly children? They probably won’t do anything with it except put it in a retirement account. Life satisfaction upgrade = 0.

How I’m Thinking About This

I’m fascinated with people’s relationship with money because it is often so deeply linked to people’s relationship with work. Show me your insecurities around money and I’ll show you your potential for thriving.

Most of us learned some lesson about money from childhood that has stuck with us. We will never have enough. People with money are bad. Money is the most important thing in life. You will never make money. Money makes people do evil things. Money is deserved. You can go on forever.

But one of the most powerful scripts with money is around when and how you should spend your money during your life. Almost everyone has the same strategy. Save as much as possible for retirement.

Perkins’s book has persuaded me that I might be making this mistake and saving too aggressively for retirement – a time in which my health will be worse, my spending habits will be tamer, and my desires to travel will likely be less enthusiastic.

The book was inspiring and it’s pushed me to think deeply about how I can spend more intentionally on creating life experiences with my family that might pay memory dividends for decades, how I can gift my children “pre-inheritance” that might enable them to live more boldly while young, and how we should move up some of our plans to integrate living abroad and travel into the next few years.

As always, you can follow along here, as I’ll be sharing what I learn along the way.

Join 25,000+ curious readers

Reflections on life, work, and what really matters