How I Think About Money & Retirement While Self Employed

The most common question I get from people who are not self-employed is about my level of worry when it comes to money. People wonder if I’m worried about the future. Worried about having “enough” for things like a house, college, and retirement.

People are often surprised at two things that emerge from a deeper exploration of this topic:

- How little they’ve really analyzed their own relationship to money

- How deeply I have thought about it

One of the surprising things of self-employment is that it forces you to face your money fears immediately and because of the unpredictable nature of income flows over time, forces you to develop a working mental model of how to think about money. This is in contrast to many full-time employees who because of steady income flows can put off ever having a coherent framework for thinking about money as long as they stay employed.

What follows are some of the principles I have adopted for how I think about money. Remember this works well for me and might not work for you.

Belief #1: Financial insecurity can’t be “cured” by making more money

Financial insecurity seems to be a proxy for all sorts of insecurities including a general fear of death, the general anxiety of rising costs of the modern world and feeling like you’ll run out of money, and not feeling like you are good enough.

Financial insecurity appears in different forms and has varying level of costs. For some it is a hacking of their brain in the form of a daily refresh of a Mint.com or personal capital profile. For others it is the explicit cost of hiring a financial advisor and paying them 1% of annual assets. For others it can be a desperation to take and stay at any job that will take them regardless if it makes your life better. This insecurity led to me becoming desperate when looking for consulting work a few times when income streams had dried up which led to underpricing or taking project that were not a great fit.

Most people try to quiet these insecurities by making more money, getting another gig, or sometimes, investing in riskier things. It never gets rid of those voices, it only quiets them. I made good money while I was employed but was surprised at how potent some of my hidden insecurities were when I quit my job.

This is why taking a break for employment or earning less money is often one of the most counterintuitive and effective ways to grapple with financial insecurity.

When I first moved to Taiwan my consulting work dried up and I made about $500 over a stretch of 4-5 months. In response I cut my spending dramatically and I learned two things: I didn’t need much to be happy and I could radically re-arrange my cost of living pretty in less time than I thought.

This did not cure my financial insecurity completely but it just made me more comfortable with the feeling and instead of letting it hack my decision making processes I could practice sitting with the discomfort.

Another thing people do when they think about quitting their job is frame it as an all-or-nothing leap. It’s either go into the risky path of self-employment or stay in full-time work forever.

Going “back” to salaried employment is often much easier than people imagine and what people really fear is that people will not accept them anymore. If I decided to go back to full-time employment I am much more confident I’d be able to find work and an arrangement that would work for me because of what I’ve learned over the past few years.

The reality is that most self-employed people like it and don’t want to go “back.”

Belief #2: People will spend years avoiding discomfort

People go to enormous lengths to avoid having to face these emotions directly and this is what makes quitting full-time employment so terrifying. It is not the prospect of going broke or earning less that scares people but having to be uncomfortable for long stretches of time.

Have you ever seen someone that was a bit older and had made really good money for a while lose their job? You probably thought, “wow they have worked hard, maybe they will take some time off and regroup.” What likely happened instead was that they were aggressively job searching the next day.

What you are seeing is someone that has used full-time employment and a steady income as a way to masks deeper insecurities and discomfort.

I was lucky because a two-year health crisis threw me out of the working world. I literally had to sit with discomfort. Sitting in my bed each day I dealt with the physical discomfort of Lyme disease and also the psychological discomfort of being out of work without a paycheck and unsure of who I was.

This is something people don’t see when they look at my current path. I’ve been through some shit and gotten to the other side. I could do it again.

When I decided to quit my job I confused when people would tell me how brave I was or that they could never do such a thing because “they couldn’t pay rent.”

These statements are rarely the result of a financial analysis but instead of the paycheck mindset of one-month, one-paycheck. To imagine life without a paycheck each month is uncomfortable for people and they’d do almost anything to avoid it.

Having a steady flow of income keeps you blind to the fact that when you remove this cash flow your mind will naturally start coming up with ways to make money.

In 1944 worries about food shortages from the War started to emerge. At the University of Minnesota they recruited 36 participants to take part in a starvation study. After extended periods without food, they starting becoming obsessed with food. It was all they thought about and talked about. They planned to open restaurants, to become restaurateurs, memorized recipes, and compared food prices of different newspapers for fun.

The first few months after quitting my job I didn’t make any money. I became increasingly proactive and imaginative about ways of making money. I ended up making a lot of money over the next six months. My worries about making money receded quicker than I imagine but my deeper discomfort with how I would navigate this up and down emerged as the real issue. This is something that never goes completely away but if you start to see the potential scarcity of income as a feature that helps you grapple with this discomfort you can start to see how not leaving your job might be the risky thing to do.

Belief #3: People don’t define “enough”

Many people refuse to commit to a number or salary that is “enough” and even when they do they will often change it once they have reached that number. It is amazing how much wealth people will accumulate without ever realizing this fact. In addition, most people’s expectations of what they need are built on their current lifestyle and if you have head steadily increasing salaries and expenses you will assume it is only possible to live and be happy in such an arrangement

I’ve talked to people with millions of dollars who are convinced they are struggling. I’ve talked to people making $500,000 a year who think that they won’t be able to afford college for their kids, let alone retirement. People who say they need $1 million to retire and then when they hit it they change the number to $1.5 million.

For these people, it is impossible to ever have enough because enough is just always more than they have now. This is the result of refusing to grapple with the underlying insecurities that making more money hides.

Instead of defaulting to “more is better” I’ve tried to calculate what I have, what my ideal lifestyle cost, and try to imagine a range of possibilities and whether or not I’ll be able to make it work.

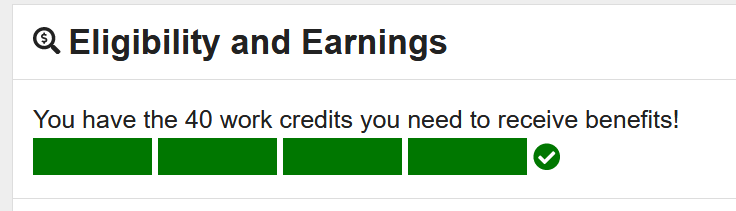

One thing I did early on in self-employment was to login to the Social Security site which gives you information about the government’s pension scheme. I was curious how much retirement I might get from something like this. I was surprised to find that I had already “fully qualified” after working for 40 quarters in my life. I had not maximized my potential payouts but I could start collecting a payment at about age 62 in the US.

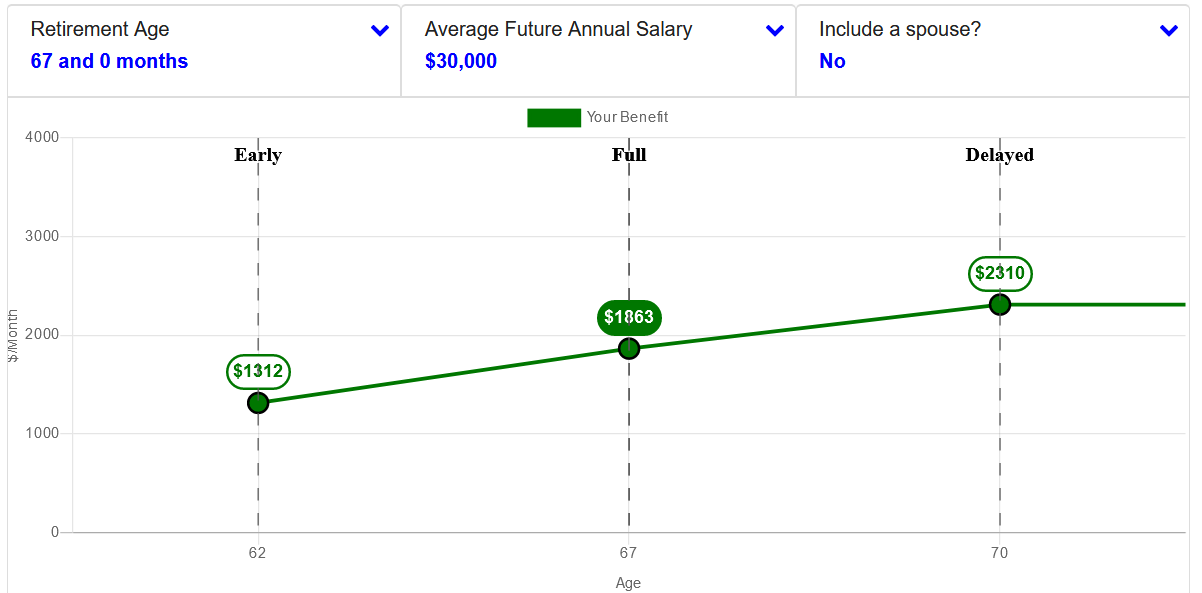

I was also surprised to find that under a worst-case scenario of needing to take money at age 62 and only making $30,000 a year until retirement (and not counting my spouse who isn’t a US resident yet), that I would received $1312 a month until I did.

That’s not bad! Especially considering that we have enjoyed living in different countries, our worst case scenario is probably a nice cushion on top of our existing retirement savings.

I’ve always invested for the future. Perhaps I knew that I’d want to leave the world of knowledge work. As soon as I started working I invested about 15-25% of all paychecks into retirement. The stock market is 4x what it was in 2009. This seems to have paid off even though I never made a crazy high income.

Right now if I project even a very conservative 4% annualized market return for the next 30 years, invested no additional money, and then took out the money and put it in cash and paid myself an annual salary for 25 years this would be an additional $3,423 per month (if you are ambitious you can figure out the details).

This puts me at a “retirement” of nearly $5,000 a month starting at age 65 based on no additional investments and that I can break even for the next 30 years.

Barring any health issues that prevent me from working I would guess that 95% of future life paths will end up better than this. Pretty cool.

To those of you that are saying that $5,000 is not enough this article is not for you. I write for the people who might want to opt for more time rather than more stuff and people who don’t want to design their lives around work.

This analysis helped me shift from a generalized worry about the future to a very clear understanding of what kind of risk I was dealing with. My risk of ruin is quite low which means I can spend a lot more time making small bets on interesting opportunities or even using my time for non-work and spending time with people I love.

I know how to make more money and one day I might change my mind and try to earn more but for not figuring out how to be happy on less money is a way more interesting game to play than trying to keep a steady income or even earn as much as possible.

I think that we can have a pretty good life in most parts of the world, even with kids, making $40,000-$50,000 per year. The biggest challenge will likely be judgement from other people if we decide not to opt-in to the default high-priced success path of high-income knowledge workers. I don’t have kids yet so I am also happy to revisit this admit that I am wrong when that time comes.

Other people see my life as extremely risky but I see the possibility of ruin as almost zero. Defining a “worst-case” scenario enables me to leave space for opportunities to emerge or for extended periods of non-work without anxiety.

I don’t buy into the default retirement story

A lot of thinking about money and retirement comes with a default picture of work and life that says you work 40 years and then retire and live a life of leisure. This does not appeal to me. I want to be actively engaged with the world, even when older.

The current paradigm of work seems to suggest that one should suffer for a long stretch of time working full-time and then at a certain age let out a deep breath and head somewhere warm to retire and spend time with other retired people.

I am quite sure I don’t want this because I am not interested in a life of leisure, at least how people think about it now. I’m much more interested in the historical definition of leisure, one that centered around contemplation and active engagement with the world.

We’ve lost a connection to this idea of leisure because our obsession with work has drained it from our souls. The most interesting thing that has emerged for me in exploring self-employment is the shock at how much energy and enthusiasm for life has reappeared after a decade in the corporate world.

This showed up because I was actively engaging in the world in many different modes. I’ve worked in many different types of gigs and volunteered and spent extended time with important people in my life. My imagination for the possibilities for my life and work have expanded exponentially. When I think about the latter stages of my life I think about how I can continue to do the things that matter to me, writing, teaching, and mentoring in various capacities.

The modern idea of retirement is tied to the idea that work is suffering and that retirement is a relief. While I don’t see work as the most important thing in my life, I also don’t see it as the worst. Thus I likely see it playing some role in my life. Whether I try to make money from those modes of being or not will depend on my needs but I hope it will be the latter.

The other major fear that drives people to follow this script is healthcare. I come from the only first world third world country when it comes to healthcare. I’ll write a bit more about this below but my country is one of the few that regularly bankrupts its citizens who have health issues that are out of their control.

However, we’ve already talked about how making more money is never going to solve the fear of not having enough money. Combine this with a real health crisis I faced in my twenties and I know that compromising parts of your life for future potential worries is just not worth it. I’ve heard too many horror stories of people facing health crisis right after retiring and never getting to live out their dreams.

This is why I think much more about “pre-retirement” experiences like extended vacations with family members and friends now rather than in 30 years wen my health, energy levels and ability to deal with discomfort (and cheap hotels) will be much resilient. Since I plan to always do different types of work I don’t think I’ll be resentful if I have to do work later if I need money.

I rather steal minutes from today and lose money in the future. If I run out of money I know that I can figure it out.

I had a weird experience in Mexico last year when I found myself in a tropical location, watching beautiful sunsets every night with my wife, working a few hours a day and being quite happy. I thought to myself, “this is the goal of retirement people aim towards, huh.”

The bigger challenge with this in mind is what I aim towards instead of a traditional retirement? The simple answer is that I’m not aiming towards anything. I’m trying to be fully alive today.

The Largest Uncertainty: “What about healthcare??”

Healthcare in the US is an absolute dumpster fire and probably is the most valid reason for worrying about the future.

I do worry about the future of healthcare and my ability to afford it but I also don’t see it as a good enough reason to re-orient my life around making as much money as possible through full-time employment.

After dealing with complicated dental issues, nerve damage, getting bit by a dog, an intestinal parasite, and an ear infection while traveling around the world it has eased some of my worries of being able to pay for healthcare.

The best argument for getting super rich is so that you can get access to the best doctors and pay for expensive treatments. However, this is a very American issue. Since my wife is from another country and I am comfortable getting healthcare in other countries, I’d be okay with living outside of the US even when old (or for our generation, maybe especially when old!)

If the US healthcare system is not fixed in the next 30 years we will have much worse problems. Many people are holding off on their dreams because of this and it kills me. I’m not willing to let a broken system shape the course of my life.

Join 25,000+ curious readers

Reflections on life, work, and what really matters